Dagcoin is the first cryptocurrency designed for using, not trading – exactly the way money is supposed to be!

Dagcoin and the future of currencies

We believe that cryptocurrencies are here to be a step up from regular money. This means improving the speed of transactions while reducing the cost, giving access to money to more people with lesser restrictions and limitations, giving more freedom to transact. And at the same time preventing fraud and illegal activities. Dagcoin was created to fulfil all of these criterias – to become a digital version of money that people can use all around the world.

Near-zero transaction fees

Fixed transparent transaction fee without any hidden fees or exchange rates. Does not matter whether sending 10 or 10 000 dags, the cost will always be around 0.0005 dagcoins.

Almost instant transactions

Regular transactions can take from days to weeks, several cryptocurrencies can take from tens of minutes to hours. Dagcoin transactions are fully confirmed within 30 seconds on average.

Freedom to transact

People around the world have the freedom to make fast and cost-effective transactions with their Dagcoin wallets. No limits, no restrictions. You have control over your money.

Licensed cryptocurrency

Dagcoin is strictly following KYC and AML laws to reduce illegal or criminal transactions in the financial world.

1000+

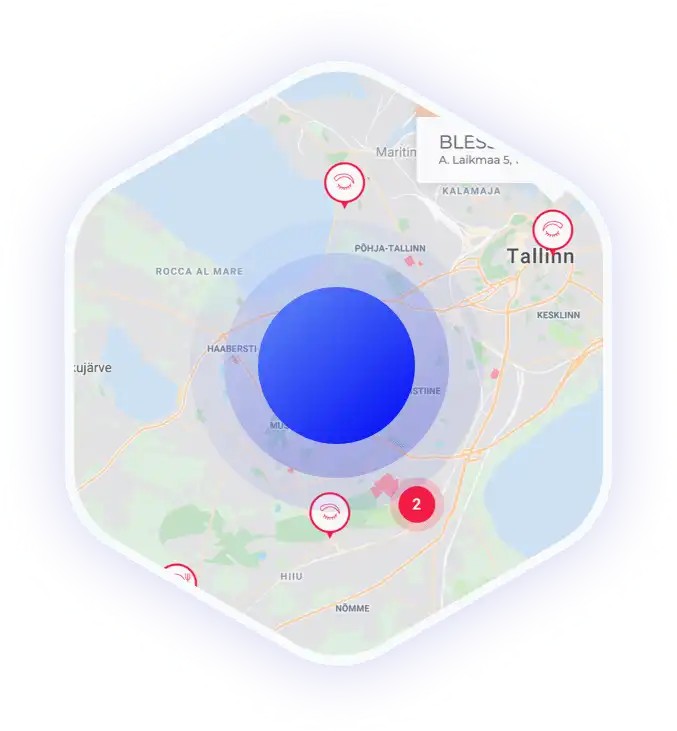

Find merchants all around the world

Dagcoin is meant for using. Everything you do with regular currency, you will be able to do with dagcoins. This includes getting paid, going shopping, exchanging, taking loans, paying for services, travelling, and almost everything else that comes to your mind.

500 000+ members

The Dagcoin community is growing rapidly all around the world. Instead of creating a group of speculating traders who are chasing the price movement, we are building an educated community of cryptocurrency supporters who understand the long-term vision and are passionate about the true value of cryptos – the reasons they were created and how people worldwide can benefit.

Quick specs and the whitepaper

| Technology: | DAG-chain |

| Transaction fee: | Around 0.0005 DAG |

| Avg transaction time: | 30 seconds on average |

| Total supply: | 9 000 000 000 dags |

| Coin distribution: | 5% – team, founders, advisors 95% – community |

| Distributed coins: | 3B dags |

| Reserved coins: | 6B |

| Available in (exchange) | LBank |

The 3-step strategy for growth

Create an ecosystem

The biggest innovators are flexible and can adapt to changes faster than the industry giants. It takes a while for the biggest companies to start accepting cryptocurrency. The best way to start is by creating an ecosystem and build the main products and services ourselves.

Build the community

Once the ecosystem has been developed, we will grow the community and integrate the products and services into our everyday lives. A currency becomes strong once people and businesses start trusting and using it. We can show the world how cryptocurrency is truly meant to be used.

Scale & co-operate

Scaling the community to millions of people assures that the ecosystem is working and gives insight for perfecting the products. This is required in order to begin cooperating with the biggest brands in the world, eventually leading to mass adoption.